Geneva – The International Air Transport Association (IATA) announced global passenger traffic results for February showing a second month of strong demand growth to begin 2017.

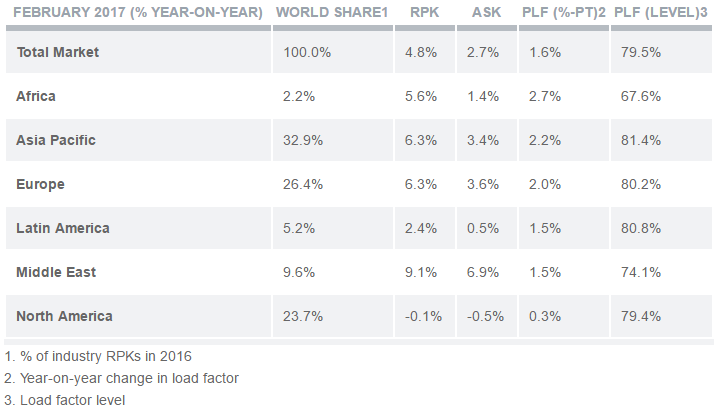

Total revenue passenger kilometers (RPKs) rose 4.8%, compared to the same month last year. Although this was below growth achieved in January, year-to-year comparisons are distorted because February 2016 was a leap month. Adjusting for the one fewer day this year, the underlying growth rate was estimated at 8.6%, just under January’s increase of 8.9%. Monthly capacity (available seat kilometers or ASKs) increased by 2.7%, and load factor rose 1.6 percentage points to 79.5%, which was the highest ever recorded for February.

“The strong demand momentum from January has continued, supported by lower fares and a healthier economic backdrop. Although we remain concerned over the impact of any travel restrictions or closing of borders, we have not seen the attempted US ban on travel from six countries translate into an identifiable traffic trend. Overall travel demand continues to grow at a robust rate,” said Alexandre de Juniac, IATA’s Director General and CEO.

IATA estimates that allowing for inflation, the price of air travel has fallen by more than 10% in real terms over the past year, accounting for more than half the growth in RPKs in early 2017.

February international passenger demand rose 5.8% compared to February 2016, which was down compared to the 9.1% yearly increase recorded in January. Adjusting for the leap year, however, growth actually accelerated slightly compared to January. Total capacity climbed 3.4%, and load factor rose 1.8 percentage points to 78.4%.

European carriers saw February demand increase by 6.5% compared to a year ago. Traffic has resumed its growth after the terrorist disruptions in 2016, supported in part by momentum in the regional economy. Capacity climbed 3.4% and load factor surged 2.4 percentage points to 81.1%.

Asia-Pacific airlines’ February traffic rose 5.2% compared to the year-ago period, maintaining the strong momentum of the past few months. Intra-Asia traffic remains robust and conditions on the Asia-Europe route have continued to recover from last year’s terrorism-related slowdown. Capacity increased 2.9% and load factor climbed 1.7 percentage points to 79.8%.

Middle East carriers had the strongest growth, with a 9.5% demand increase in February compared to a year ago. Capacity rose 7% and load factor climbed for a fourth consecutive month to 74.3%, up 1.8 percentage points over last year.

North American airlines’ traffic climbed 0.3%, which was the slowest among the regions. However, adjusting for the leap year, growth was estimated at 3.4%. Traffic to/ from Asia continues to move upward but transatlantic demand has trended sideways since mid-2016. Capacity inched up 0.1% and load factor edged up 0.1 percentage point to 75.9%.

Latin American airlines saw February traffic rise 5.9% compared to February 2016. Capacity increased by 2.8%, boosting load factor 2.3 percentage points to 81.4%, highest among the regions. Robust international demand within South America is offsetting weaker traffic to North America, which has trended downward since mid-2015 and fell by 3.4% in January, the most recent month for which route-specific results are available.

African airlines continued their recovery, with February traffic up 7.1% compared to a year ago. This mainly reflects the upturn on the key route to/from Europe, offsetting struggles in the region’s biggest economies of Nigeria and South Africa. Capacity rose 2.3%, and load factor jumped 2.9 percentage points to 66.0%.

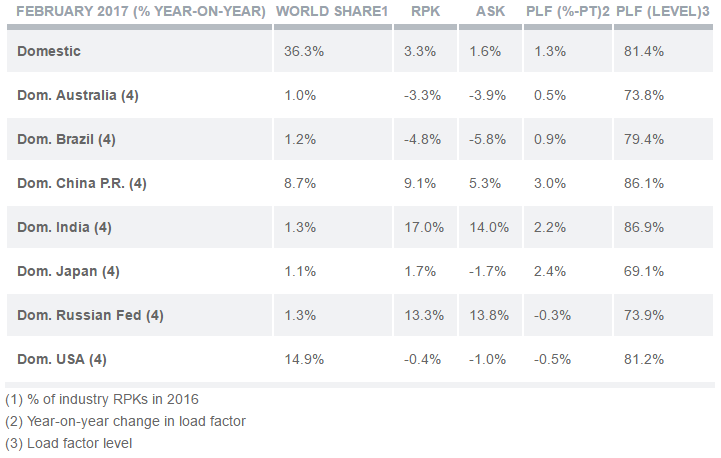

Domestic Passenger Markets

Domestic travel demand rose 3.3% in February compared to February 2016, reduced from 8.7% in January, but again, the leap year effect greatly exaggerated the slowdown. Results varied widely as Australia, Brazil and the US all registered non-adjusted declines. Domestic capacity climbed 1.6%, and load factor increased 1.3 percentage points to 81.4%.

The Bottom Line

The year has opened with some shocks—the attempted ban on travel to the US by citizens of six countries and the restrictions on the carry-on of large electronic items from certain airports in the Middle East and North Africa on direct flights to the US and the UK. The potential implications of the Brexit talks on the air transport industry are significant and the political rhetoric of protectionism and closing of borders is adding to the ambiguity.

“It’s intolerable that governments continue to add to the uncertainties facing the air transport industry by failing to engage airline operational know-how on issues that can damage public confidence. The introduction of restrictions on the carry-on of large electronic devices was a missed opportunity and the result was a measure that cannot stand-up to the scrutiny of public confidence in the long term. Although Australia’s measures were also implemented without consulting the industry, they at least demonstrate the potential to mitigate the threat with less disruptive means. We all want to keep flying secure. And we can do that most effectively by working together,” said de Juniac.

In tandem, states need to support the International Civil Aviation Organization (ICAO) as it develops a Global Aviation Security Plan. Additionally, next month, ICAO member states will consider amendments to Annex 17 of the Chicago Convention that would require information sharing. “The security experience of recent years should compel states to support this,” said de Juniac.