Popular Bank’s commercial real estate approach has zeroed in on two distinct lending options: bridge lending and construction financing. The bank’s team helps clients, including local developers and investors, understand which option to use and when, helping them unlock opportunities in one of the nation’s hottest markets.

Bridge Lending: a phased approach to financing construction projects

The bridge lending market has transformed dramatically in recent months. Less than two years ago, the rates were in double digits. The rate has since dropped below 10%, making bridge lending a more attractive and accessible capital option for borrowers.

For developers pursuing repositioning or stabilization plays, bridge loans present a window of opportunity. For some clients, a phased approach tied to specific project deliverables makes the most sense. A few weeks ago, Popular Bank closed a $10 Million bridge loan to help finalize renovations and lease-up of a 71-unit multifamily building in the Little Havana neighborhood of Miami. Working closely with the client, the bank defined each stage of the project, outlining what needed to be completed to activate the next funding found. Access to multi-phased short-term capital kept the project momentum going while mitigating the risks of larger financing loans. It was the right approach for the project and it is currently in phase two of funding their project.

Construction Lending: financing ground-up projects from blueprint to occupancy

For developers considering a construction loan, it is important to keep a few things top of mind. Unlike shorter-phased bridge loans, capacity in construction lending has tightened. Lenders and developers alike are looking at project feasibility before breaking ground. Regulatory pressures, higher costs of labor and materials, concentration limits, and sector-specific stress have made lenders far more selective, particularly for speculative builds.

And while Miami’s market fundamentals remain strong, they can vary by property type. Multifamily faces short-term pressure with more than 32,000 units under construction, about 24% of existing supply. Industrial vacancy has risen to 6.2% following record deliveries. Retail continues to perform well with sub-4% vacancy and limited new inventory.

For condominium developers, lender expectations have increased as well, often requiring significant pre-sale levels before a construction loan closes. These higher thresholds help ensure projects demonstrate true market demand in a segment where sales velocity varies widely by location and product type. Popular Bank recently helped finance a ground-up construction of a 312-unit multifamily located in the Naranja neighborhood of Miami-Dade with a $32.4 Million loan.

Miami remains one of the most dynamic commercial real estate markets in the nation, with tens of thousands of jobs added in the past two years alone. The opportunity is here and lenders like Popular Bank remain eager to deploy capital for well-positioned projects that make our city vibrant and enjoyable for everyone.

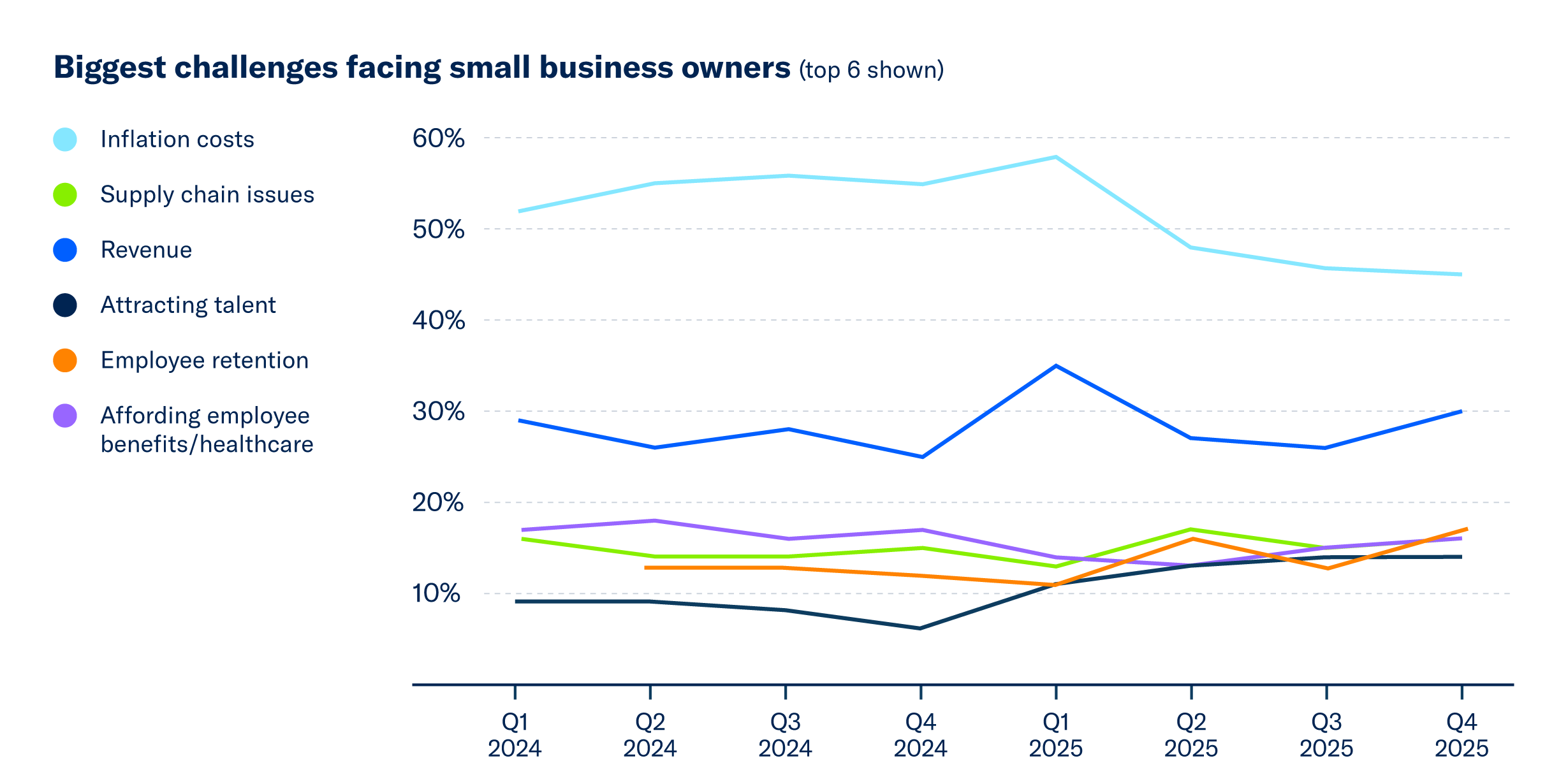

The latest MetLife & U.S. Chamber of Commerce Small Business Index shows that employers’ concerns about recruiting and retaining workers have been rising over the past year.

The survey also shows that inflation is stubbornly lingering as the top concern for small businesses, despite receding slightly from record highs.

This quarter, the Index shows that small businesses’ concern about their ability to retain employees (17%) and attract talent (14%) is rising. Roughly one in four (26%) small business owners select one of these “talent” items as their top concern.

Concerns Over Talent Rise

Concerns over attracting talent has risen eight percentage points compared to this time last year (was 6% in Q4 2024). Similarly, retaining employees has risen five percentage points over the same time period (was 12% in Q4 2024).

“This quarter’s Index makes it clear: attracting and retaining employees is a growing concern for today’s small businesses,” said Bradd Chignoli, executive vice president and head of Regional Business & Workforce Engagement at MetLife.

Notably, the percentage of small businesses that selected either retaining employees or attracting talent has risen from 16% in Q4 2024 to 26% this quarter. [1]

[1]In Q4 2024, this option was asked as “Lack of applicants for job openings”.

Lower levels of concern about talent also existed three years ago. In Q4 2022, 11% of small businesses considered employee retention a top concern and just 8% said attracting talent was a top concern.

Inflation Concerns Small Retailers Most

This quarter’s survey also shows that inflation remains the top concern among small business owners: 45% say it is the biggest challenge they face right now. However, concern has remained below the 50% threshold for a third consecutive quarter and is on par with Q2 2022 (44%).

“Inflation remains the top challenge, and workforce concerns are rising,” said Tom Sullivan, Senior Vice President of Small Business Policy at the U.S. Chamber of Commerce. “Yet, small businesses are showing resilience, even amid uncertainty exacerbated by the longest government shutdown in history, when this survey was in the field.”

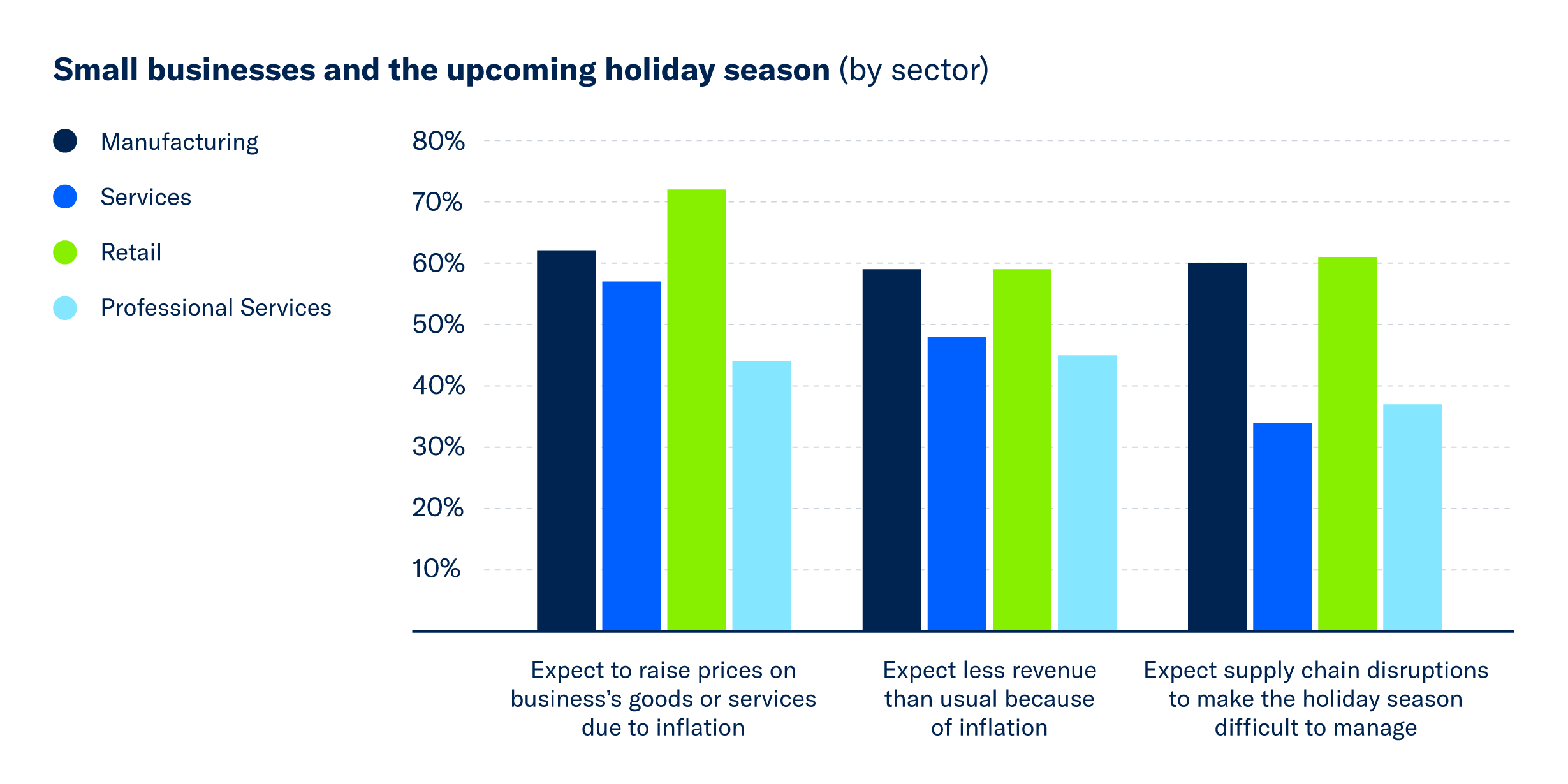

But all sectors are not equal when it comes to inflation concerns. In fact, small retailers are the most worried about inflation with 53% saying it’s a top concern. Manufacturers are least concerned about inflation (38% said it was a top concern). In the middle: 46% in the services industry and 42% in professional services said inflation is their top concern.

Small businesses also report that inflation is impacting their holiday plans. Over half (58%) expect to raise prices, and 52% anticipate lower revenue due to inflation.

Minority-owned businesses (55%) and small businesses with 20-500 employees (53%) also express higher levels of concern over inflation. Smaller small businesses are less concerned about inflation: Both 44% of medium (5-19 employees) and the smallest small businesses (1-4 employees) cite inflation as a top concern.

Similarly, concerns about revenue saw a slight uptick this quarter from 26% to 30% and remain relatively high. Revenue concerns now sit at the second highest level since 2021, only beat by Q1 2025 (35%).

]]>

The recently enacted “One Big Beautiful Bill Act” includes substantial tax reforms to support the growth of small businesses. Small business owners can take advantage of these tax breaks starting now for expenses dating back to January 20, 2025.

This guide outlines the most impactful provisions of the law, including permanent deductions, enhanced credits, and expanded eligibility criteria. It provides clear, step-by-step instructions to help business owners navigate the changes and optimize their tax strategies. Download the guide or read below to learn more.

1. Permanently Claim the 20% Qualified Business Income (QBI) Deduction

Who qualifies: Sole proprietors, partners, and S corporation shareholders.

What to do:

- Calculate your qualified business income (QBI) for the year.

- Deduct 20% of your QBI on your federal tax return every year—this deduction is now permanent.

- If your QBI deduction is low, check your eligibility for the new inflation-adjusted minimum deduction (at least $400).

- If you were previously ineligible for the deduction, determine whether changes to the phase-in of existing limitations make your business eligible.

Action item:

Work with your accountant or tax professional to determine your eligibility and claim the maximum deduction each year.

2. Immediately Deduct Qualifying Research & Experimental (R&E) Expenses

Who qualifies: Businesses with domestic R&E spending, especially those with average annual gross receipts of $31 million or less.

What to do:

- Track your U.S.-based R&E expenses each year.

- Deduct 100% of your qualifying R&E expenses this year on your 2025 tax return.

- If your annual gross receipts average $31 million or less, you may apply this benefit retroactively for tax years 2022–2024.

Action item:

Review past returns with your tax professional to seek retroactive refunds if eligible.

]]>

Even after this year, the One Big Beautiful Bill Act will continue to help small businesses because Congress made the 20% small business deduction and these changes permanent. Permanency provides the clarity and stability businesses need to plan confidently for the future, ensuring they can reinvest in their workforce, expand operations, and drive economic growth.

Unleashing Growth Through R&D Expensing

The 2025 law’s restoration of immediate expensing for U.S.-based R&D costs stands as a major victory for American innovation.

As Natalie Kaddas, CEO of Kaddas Enterprises in Utah, explains: re-instatement of immediate R&D expensing lifts a punishing tax burden that stifled investment for the past three years when companies were forced to amortize R&D costs—tying up much-needed capital. Kaddas Enterprises faced a 35% effective tax hike for each year they were forced to amortize R&D instead of expensing it immediately. Now, freed from this drag on cash flow, small firms can invest in operational upgrades and energy-resiliency efforts, fueling progress that benefits local communities and the national economy.

Victoria Thomas, President of VICCI Inc., echoes this sentiment from Wisconsin’s motorsports industry. By allowing business owners to amend tax returns for refunds on previously amortized R&D, her team is unlocking more than six figures to grow, hire, and innovate. It’s not simply about balance sheets; it’s direct evidence that the tax change incentivizes American manufacturing and supports Thomas’s strategic partners like Riley Technologies, which is already experiencing a surge in custom, high-performance car orders for 2026.

Making Productivity Investments Possible

The new tax law’s impact isn’t limited to research—it also directly addresses capital investment and productivity.

Traci Tapani, co-owner of Wyoming Machine in Minnesota, provides an example of how the law’s 100% bonus depreciation for new equipment creates opportunity and reduces risk. Before this reform, smaller manufacturers could deduct only 40% of the cost of major technology purchases in the first year and 20% in the second. The new rules allow full deduction up front, whether investing in cutting-edge fiber optic laser welding or other advanced tools.

For Tapani, the purchase of a new fiber optic laser welding machine, enabled by passage of the One Big Beautiful Bill Act, not only boosts productivity but also addresses chronic shortages in highly trained welders. Fiber optic welding is easier to use and less damaging to materials, allowing Wyoming Machine to serve a wider array of customers and industries.

Clarity and Confidence for Growth

Perhaps the most underrated gift of the One Big Beautiful Bill Act is confidence—clear, permanent rules that help business owners plan for the future.

As Mike Zaffaroni of Liberty Landscape Supply in Jacksonville, Florida, explains, uncertainties over whether a small business deduction for sole proprietors, partnerships, and S corporations would be extended beyond the end of this year made long-term decisions difficult. The new tax law made that 20% small business deduction permanent and put an end to this anxiety. The permanent restoration of 100% bonus depreciation and the deduction for R&D costs are also helping Zaffaroni turn wish-list projects into business realities—like a $100,000 upgrade in enterprise software, truck purchases, and new hires to meet customer demand.

When small businesses can plan ahead, they invest, expand, and hire. That ripple effect strengthens communities and helps secure America’s economic leadership.

]]>

Use the guide below to discover the value that an HOA money market account (MMA) can bring to your association’s reserve funds

How can money market accounts benefit community and homeowners associations?

Money market accounts can help community associations and HOAs manage their reserve funds more effectively by keeping reserve and operating funds separate. Unlike certificates of deposit (CDs), these accounts typically offer more liquidity, allowing boards to access funds without disrupting long-term planning. This balance of accessibility and stability supports an HOA’s fiduciary responsibility to protect member funds.

Money market accounts are interest-bearing accounts that allow an association’s reserve funds to earn a competitive rate. These accounts often have higher interest rates than traditional savings accounts, and tiered interest rates also unlock a higher return on investment, given that an HOA’s reserve fund tends to be larger than what your average individual money market account holder might have at their disposal.

Funds held in a money market account are insured by the Federal Deposit Insurance Corporation (FDIC) for up to $250,000 per account, similar to a checking or savings account. Although most banks limit the number of penalty-free withdrawals per statement period, community associations can plan ahead to help avoid unnecessary fees.

Funds held in a money market account are insured by the Federal Deposit Insurance Corporation (FDIC) for up to $250,000 per account, similar to a checking or savings account. Although most banks limit the number of penalty-free withdrawals per statement period, community associations can plan ahead to help avoid unnecessary fees.

How to open an HOA money market account.

Opening an association bank account requires gathering the appropriate legal documents to share with the bank and ensuring transparency with homeowners. Before opening the account, community association board members should consult the bylaws and communicate the plan to residents. The steps below outline how to open an HOA money market account.

1. Evaluate the role of the HOA money market account in managing reserve funds

Determine how much of the reserve funds will be placed within the association’s money market account. Clarify when board members or the treasurer may access funds. It may also be helpful to establish future goals for the reserve fund and interest earnings.

2. Research and compare available money market accounts

Explore different money market account options and review how each one aligns with the association’s financial goals. Compare features, benefits, and potential drawbacks to help identify which accounts support your needs, both present and future.

3. Gather necessary documents

Review the application requirements for the money market account you want to open. Gather any necessary documents, such as the bylaws and other governing documents, the association’s Employer Identification Number (EIN), applicable board meeting minutes, authorized signers, and any other paperwork required. Meet with a Relationship Manager to open the account after deciding who from the HOA will be involved in managing the account.

4. Fund and maintain the account

Meet the minimum opening balance requirements for the money market account and make a plan for ongoing contributions. Review account activity and performance at routine board meetings to ensure the account continues to support the association’s financial strategy.

What to look for in an HOA money market account.

Reviewing only the numbers advertised with money market accounts can lead to a misalignment between the HOA’s financial goals and the account’s characteristics. However, evaluating potential money market accounts through the lens of the following features can help HOAs make a more informed decision:

- Account terms and conditions: Review the fine print to understand any withdrawal restrictions, transaction limits, or requirements necessary to maintain the advertised interest rate.

- Interest rates: Compare both introductory and ongoing rates, and note whether they’re fixed, variable, or change on a set schedule.

- Applicable fees: Identify any monthly maintenance fees, transaction fees, or penalties that could reduce earnings.

- Minimum balance requirements: Note the minimum opening deposit and any continuing balance thresholds necessary for avoiding penalties.

- Accessibility: Consider how easy it is to access funds via checks, electronic transfers, or in-person withdrawals. Also, determine if the account can be managed online or through a mobile app.

- FDIC insurance: Most banks offer this insurance—up to $250,000 per account—but it’s a good rule of thumb to confirm it’s included.

The best money market accounts also offer superior customer service and ongoing account support. Keep these factors in mind when comparing accounts to find the best option for your HOA or community association.

HOA money market account best practices

Once the account is opened, it should be managed using the same standards and procedures of all HOA funds. For instance, the treasurer typically oversees the account and money management, but the board should maintain shared responsibility. Additional best practices include:

- Using reserve funds only when approved by the bylaws, homeowners, and the board

- Reviewing accounts annually to ensure the association is benefitting from competitive rates and reliable customer service

- Ensuring the account meets requirements to avoid fees, such as maintaining minimum balances or limiting withdrawals per statement period

- Conducting regular audits to reduce the risk of fraud

Maximize the potential of your reserve funds

Community associations of all types—HOAs, condos, and co-ops—can benefit from careful reserve fund planning. Working with a banker who understands the needs of community associations can help you identify options that will support long-term financial stability. Contact Popular Association Banking today to learn more about how a money market account may support your association’s goals.

]]>- IMF staff and the Honduran authorities have reached staff-level agreement on policies and reforms to complete the fourth reviews of the Extended Fund Facility (EFF) and Extended Credit Facility (ECF) arrangements. IMF Board approval of the review, expected for later this year, would result in a disbursement of about US$120 million.

- The Honduran economy remains resilient, and the authorities continue to make solid progress implementing their economic program, with a healthy accumulation of international reserves. Solid economic growth, anchored inflation, and an improved external position reflect prudent fiscal management and decisive monetary and exchange rate policies which have allowed the economy to continue to rebalance.

- Maintaining prudent and consistent macroeconomic policies amid elevated uncertainty is essential to safeguarding stability. Resolute and sustained efforts to implement key structural reforms remain critical to medium-term prospects for inclusive and equitable development. Continued progress to strengthen transparency and governance ahead of the 2026 Financial Action Task Force (FATF) evaluation is paramount.

Tegucigalpa, Honduras: An International Monetary Fund (IMF) team led by Emilio Fernandez Corugedo visited Tegucigalpa from September 16 to 26, 2025, to discuss recent economic developments and policy implementation. At the conclusion of the visit, Mr. Fernandez Corugedo issued the following statement:

“The Honduran authorities and the IMF team have reached staff-level agreement to complete the fourth reviews of the Extended Credit Facility (ECF) and Extended Fund Facility (EFF) arrangements. The IMF’s Executive Board is expected to consider the case later this year.

“The team and the authorities agreed that strong economic policies, a surge in remittances, and favorable export prices have allowed Honduras to continue to navigate successfully this period of exceptional global uncertainty and in the context of an election year. Macroeconomic policy performance has remained strong and supportive of program objectives. Economic activity indicators point to robust growth of 3.9 percent in the first half of 2025. Headline inflation, at 4.2 percent in August, has remained within the tolerance range of the Central Bank of Honduras’ (BCH’s) inflation objective, while core and services inflation remain modestly higher. International reserves have increased to US$9.7 billion, appropriately strengthening Honduras’ external buffers amid a challenging global environment.

“The authorities have redoubled efforts in the implementation of their structural agenda, achieving important milestones and regaining traction in key areas. Notably, advances have been made in support of structural fiscal reforms, including measures to strengthen transparency and governance to support preparations for the 2026 Financial Action Task Force (FATF) evaluation. Likewise, the authorities, with the National Electric Power Company (ENEE), continue to lay the ground for the critical long-term international energy tender planned for early 2026.

“The authorities reiterated their strong commitment to a prudent macroeconomic policy mix. They remain vigilant and ready to act in the current uncertain global environment to ensure success of their economic program supported by the IMF. Discussions focused on policies to preserve macroeconomic stability, strengthen resilience, and bolster inclusive growth:

“First, continued fiscal prudence remains essential to safeguard macroeconomic stability, including during the election year. The 2025 deficit target of 1.5 percent of GDP remains appropriate and continues to allow additional space for productive and social investment. Consistent with program objectives, the draft 2026 budget submitted to Congress targets a 1 percent of GDP fiscal deficit, with capital expenditures above and priority social spending similar to the 2025 budget. The authorities reiterated their commitment to their structural fiscal reform agenda, including reductions in tax exemptions and strengthening public procurement, while recognizing that reprogramming some milestones may be required.

“Second, sustained efforts remain important to underpin social spending. Achievement of the June priority social spending target and completion of the urban census of poor households are welcome, with the latter allowing expansion of social support to more vulnerable families. Social spending targets for the remainder of the year are on track, and the authorities are advancing complementary interventions and digitalization initiatives. Continued efforts are needed on the Single Social Sector Information System (SUISS), whose completion has faced interoperability challenges. The production of a manual to guide temporary social assistance in emergencies, to help more effectively cushion families affected by weather-related shocks, is on track for the end of the year.

“Third, the BCH will continue its vigilant data-driven approach to maintain inflation within its tolerance range and build further buffers. Adjustments to monetary and exchange rate policies have yielded strong results and helped achieve balance between supply and demand in the FX auction. Supported by these policies, which have restored a positive differential with international interest rates, the real effective exchange rate has continued to adjust under the crawling band regime, underpinning external stability. The BCH is simplifying documentation and monitoring requirements for the FX auction, which should pragmatically improve the efficiency of the current system of FX allocation. The authorities agreed on the importance of taking further advantage of the unprecedented surge in remittances and favorable terms of trade to continue to accumulate reserves and further strengthen the external position amid an uncertain external environment.

“Fourth, redoubling efforts to maintain reform momentum in the energy sector is critical. The authorities are deploying measures to enhance loss reduction and ensure that a downward trend remains firmly established. Reducing payment arrears to energy generators and securing loans to refinance costly credit lines are key to continue strengthening ENEE’s financial position. These measures would contribute to the success of the 1,500 MW generation tender planned for early 2026, already supported by a credit line of US$ 300 million approved by the Central American Bank for Economic Integration (CABEI). Steadfast implementation of reforms to strengthen ENEE’s efficiency is essential, including aligning its accounting practices with international standards and consolidating distribution entities. Moreover, enhanced transparency through the planned publication of the 2021-23 financial audits, alongside that of a high-level online dashboard of key energy sector performance indicators, could further bolster investor confidence.

“Fifth, the authorities should continue reforms to combat corruption, improve the business environment, and strengthen governance. Ahead of the 2026 evaluation by the Financial Action Task Force (FATF), it is critical that the authorities prioritize, advance, and implement legislation addressing beneficial ownership and introducing legal amendments to further improve the Anti-Money Laundering and Countering the Financing of Terrorism (AML/CFT) framework. Efforts are also taking shape to modernize further the tax administration through projects on electronic billing and timely refunds and to strengthen public investment management with support from development partners. The authorities are developing a new whistleblower law and related reporting mechanisms and are committed to approving the Honduran National Transparency and Anti-Corruption Strategy (ENTAH).

“The IMF team would like to thank the authorities, the private sector, and other counterparts for their kind hospitality and candid discussions.”

]]>To overcome these challenges in El Salvador, IDB Lab and IDB Invest have joined forces with Banco Cuscatlán to design and implement the “LET’S DIGITAL PYME” initiative, which promotes digital transformation in this sector.

This initiative aims to transform traditional support for SMEs into a holistic approach that encompasses financial and business-related non-financial needs.

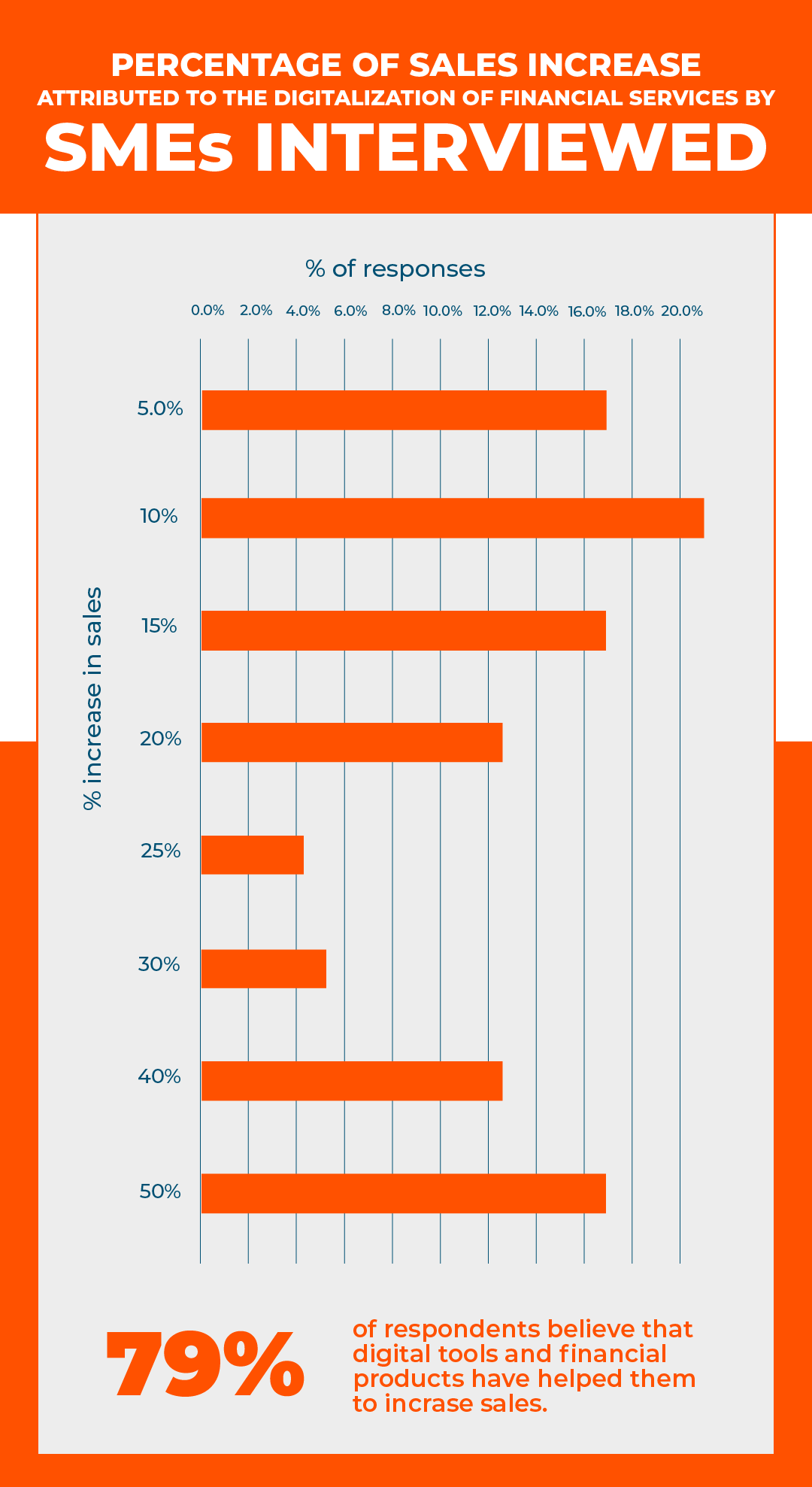

With this effort, it was possible to strengthen Salvadoran small and medium-sized enterprises in digitalization, achieving significant results:

- 79% of SMEs increased their sales between 5% and 50% (according to interviews conducted with SMEs).

- 85% reduced their operating costs.

- Ten thousand small and micro-entrepreneurs used a digital financial education platform.

- More than 3,200 women entrepreneurs received financial training.

- They incorporated digital tools and financial and non-financial products into their operations.

- All SMEs are linked to the innovation ecosystem and interested in deepening digital business transformation.

This collaboration demonstrates the synergy between the IDB Group’s private windows. With a loan operation led by IDB Invest and a technical cooperation led by IDB Lab, Banco Cuscatlán’s digital factory developed digital products for SMEs.

In turn, an open innovation challenge was carried out to address four challenges facing SMEs in digital transformation. This call attracted more than 84 applications from Startups and Fintechs from all over Latin America under a sandbox dynamic.

The finalist Fintechs and Startups could pitch and present their innovation proposals to Banco Cuscatlán. The competitive process resulted in the selection of the startups Alfi from Peru, Expediente Azul from Mexico, and FINDEX from El Salvador to integrate their solutions into Banco Cuscatlán’s platform.

From this process, valuable tools emerged from the innovation ecosystem to address specific challenges of SME clients and non-clients of the institution. These were the solutions the linked Startups created:

- Expediente Azul implemented a digital document management solution that facilitates SMEs’ administrative process optimization and access to credit.

- Alfi, for its part, was selected to address the financial education challenge and has launched an AI-based platform offering interactive and entertaining educational content to strengthen the financial management of SME entrepreneurs and entrepreneurs.

- FINDEX with an integrated solution for the administrative-financial management of businesses and the generation of electronic invoices to deepen the digitalization of SMEs.

SMEs and the Economy

Banco Cuscatlán’s support for SMEs has so far mainly focused on providing access to financing, but LET’S DIGITAL PYME has shown how SMEs can benefit from access to services offered by a bank to improve their management, operational efficiency, and technology adoption.

An important conclusion is that banks and other financial service providers must expand their offerings to include non-financial services such as training programs, mentoring, digital marketing support, and resource management tools to strengthen their business capabilities.

Therefore, financial institutions in the region, as Banco Cuscatlán has done in El Salvador, have the potential to play a fundamental role in the growth and development of the SME segment. IDB Invest and IDB Lab remain committed to collaborating with crucial and strategic actors to promote the region’s progress and the digitalization of SMEs.

Through initiatives like this, we can improve not only their access to financing but also their business competence and capacity, helping to create leading SMEs that have a positive ripple effect on our economies and societies.

]]>On June 28, the U.S. Supreme Court overturned its 1984 landmark law precedent, Chevron v. Natural Resources Defense Council. In short, Chevron instructs courts to defer to an agency’s reasonable interpretation of an ambiguous statute. It has become the most-cited administrative law decision ever, shaping judicial review of administrative actions.

“Today’s decision is an important course correction that will help create a more predictable and stable regulatory environment,” said U.S. Chamber of Commerce President and CEO Suzanne P. Clark. “The Supreme Court’s previous deference rule allowed each new presidential administration to advance their political agendas through flip-flopping regulations and not provide consistent rules of the road for businesses to navigate, plan, and invest in the future. The Chamber will continue to urge courts to faithfully interpret statutes that govern federal agencies and to ensure federal agencies act in a reasonable and lawful manner.”

The Supreme Court revisited Chevron in two companion cases—Relentless v. Department of Commerce and Loper Bright Enterprises v. Raimondo. The U.S. Chamber of Commerce is committed to helping businesses navigate the implications of the Court’s decision.

The Evolution of Chevron

Chevron deference was originally conceptualized as an effort to foster respect for the U.S. Constitution’s separation of powers. In the Court’s view, requiring the judiciary to defer to federal agencies would ensure that policy decisions are left to the politically accountable branches. It also would allow Congress to draw on the comparative advantages and expertise of the Executive Branch by allowing administrative agencies to fill in the gaps of complex statutes.

Over the last 40 years, the Chamber has filed many legal briefs weighing in on the scope of and limits on Chevron deference. For example, the Chamber has argued that courts should undertake a “rigorous textual analysis” of statutes and ensure that Chevron review imposes a “meaningful limitation” on agency overreach. And the Chamber has urged courts to hold that Chevron does not apply to certain agency decisions.

As the Chamber has explained in amicus briefs, Chevron deference has increasingly become unbounded. In its current form, Chevron deference poses a triple threat to the tripartite scheme of government that the Supreme Court had intended to protect. It entices Congress to abdicate its duty to make the law. It entices the Executive Branch to stray far beyond its duty to enforce the law. And it entices the judiciary to abandon its duty to say what the law is.

The Consequences of Chevron

Businesses value predictability and stability in the law. In order to make effective strategic and investment decisions, businesses must operate in a regulatory environment that remains relatively consistent over time and enables them to know their legal obligations in advance.

The current Chevron regime undermines predictability and stability for businesses because they cannot ascertain their regulatory obligations based on the laws. Rather, regulatory obligations today turn on unstable agency statutory interpretations, sometimes without any prior notice at all. This instability hampers productivity, investment, and innovation. Businesses cannot effectively plan for the future when agencies are free to unilaterally change the basic rules at any time.

The Supreme Court Overturns Chevron

In light of these concerns, the U.S. Supreme Court revisited Chevron. The Court heard arguments in January of this year in two companion cases—Relentless v. Department of Commerce and Loper Bright Enterprises v. Raimondo—to consider whether to eliminate, or at least substantially narrow, Chevron deference.

The Chamber filed an amicus curiae brief in these cases, arguing that the Supreme Court should repudiate the practice of reflexive judicial deference to agency interpretations of statutes that have arisen under today’s expansive understanding of Chevron deference. If Chevron deference can be salvaged at all, we further argued, the only path to doing so is by adhering faithfully to the separation of powers.

What Happens Next?

The Chamber stands ready to help businesses navigate this new regulatory terrain in light of the Supreme Court’s ruling. We will work closely with members to assess the impact of the decision.

The Chamber will continue to urge courts to faithfully interpret statutes that govern federal agencies and to ensure that federal agencies act in a reasonable and lawful manner.

]]>

Businesses, the economy, and the world win when inclusion and sustainability policies intertwine with project management, and there is an emphasis on stakeholder participation and a focus on vulnerable communities.

To promote this inclusion, we have identified the reasons that make it a winning strategy:

- Project Impact on Communities: Inclusion in project management is intrinsically linked to the social and environmental impact it generates. It is essential to ensure the participation of stakeholders and the communities involved in order to foster positive outcomes. Especially susceptible groups like those in rural areas, indigenous communities, or local communities in poverty. Involving these communities from the outset helps mitigate negative impacts and generate significant benefits for all involved parties.

- Sustainability Policies: A robust sustainability policy is crucial to ensure that projects are viable in the short term and contribute to the long-term well-being of communities. The policy includes plans for significant stakeholder engagement when a project may affect a community. These policies must be inclusive and consider environmental impacts as well as social and gender risks.

- Focus on Gender and Diversity: Including a gender perspective in projects is another fundamental aspect of driving inclusion. Understanding that environmental and social risks can affect different groups of people differently is crucial. This is why there have been efforts to ensure that women and diverse groups are involved in community participation processes and that their specific needs, risks, and opportunities are considered. This approach is not limited to gender but also encompasses diversity in ethnicity, disabilities, and sexual orientation.

- Diversity as an Inclusion Driver: Diversity should be integral to an organization’s sustainability policy. Women, along with other vulnerable populations such as Afro-descendants, indigenous peoples, people with disabilities, and LGBTQI+, constitute a significant portion of the population. These populations often face additional intersecting barriers and vulnerabilities, making an inclusive approach even more crucial. Addressing these barriers promotes social justice and fosters a more inclusive and sustainable economy.

- Inclusion in Rural Economy and SMEs: Inclusion should not be limited to large urban projects but extend to rural economies and small and medium-sized enterprises (SMEs). SMEs represent a significant part of the economic fabric in many regions and are often essential for providing products and services in rural areas. Ensuring these businesses have access to financing and participate in value chains is critical for effective economic inclusion.

- Inclusive Economic Transformations: Transformations towards a low-carbon and digital economy must be viewed through an inclusive lens. People are at the center of these transformations, and any economic change must consider its impact on all communities, especially the most vulnerable. Just transition and inclusive economies are vital concepts that ensure no one is left behind in the development process.

- Profitability: In addition to social and environmental benefits, the positive effect on business objectives adds to the arguments for inclusion. A diverse team is better able to execute due to the diversity of perspectives and a better understanding of the market. Furthermore, products and services designed with an inclusive perspective can better serve the needs of a wider audience, thus generating higher revenue. Investing in diversity and sustainability is both ethical and profitable.

Integrating inclusion and sustainability into project management and business models is a moral necessity and an essential strategy for long-term development. By ensuring the participation of all stakeholders and considering differentiated impacts on diverse populations, projects can generate significant benefits for both communities and businesses. Inclusion and environmental sustainability are interdependent pillars that, when implemented together, have the potential to transform our economies and societies positively.

IDB Invest Sustainability Week 2024. Click the image below to register:

While innovation and ingenuity are essential to entrepreneurship, the emergence of artificial intelligence (AI) offers enormous promise to such endeavors. According to our report, Empowering Small Business: The Impact of Technology on U.S. Small Business, almost one in four small businesses have adopted AI, citing improved performance in marketing and communications.

AI systems can not only enhance efficiency, save time, and improve decision-making across business operations, but they can also optimize resources, personalize customer experiences, and provide valuable insights on market trends.

Here’s a look at some real-world success stories of small businesses utilizing—and benefiting from—AI.

AI Assisting with Customer Acquisition and Retention

Hrag Kalebjian is incredibly grateful for the myriad of benefits AI brings to his business, Henry’s House of Coffee – a family-owned coffee roaster. When it comes to Search Engine Optimization (SEO), AI tools have been indispensable in developing product descriptions that not only meet a specific set of criteria determined by Kalebjian but also perform well on search.

As an e-commerce brand, Kalebjian is also thoroughly invested in understanding the lifetime value of his customers—how much it costs to acquire a customer, how much they are worth, and what type of discount should a specific cohort of the customer base receive.

AI tools serve as the “analytical brain” behind these data-driven insights and help Kalebjian determine appropriate marketing and customer service strategies to implement. By customizing chatbots to respond in a certain way, Kalebjian can view these and other insights through specific perspectives, such as that of a marketing expert, venture capitalist, or scientist.

By enhancing operational efficiency and customer insights, AI enables Henry’s House of Coffee to compete faster and smarter—a huge benefit for a small business.

Using ChatGPT and Other Tools for Marketing

For Kim Cook and her three daughters, starting and operating Something Sweet COOKie Dough, has been a labor of love. The family-owned, premium frozen cookie dough business continues to grow and evolve thanks in no small part to AI.

Cook noted that the backend of her business relies on various AI platforms, including ChatGPT for marketing, social media, and content development, and Shopify for inventory management and financial operations. Even the business’s co-manufacturer uses AI to measure and scale ingredients accordingly to enhance resource efficiency and eliminate waste.

AI has also been a valuable asset for customer service management since Cook and her daughters have been able to provide prerecorded videos to answer specific questions they receive from customers on their website.

Overall, Cook was quick to acknowledge the significant role AI plays in the business’s ability to remain competitive by expanding its reach and shipping capabilities.

Analyzing Data and Research with AI

Austin Milliken, founder of Aureate Capital—an independent investment bank that serves clients across multiple industries and sectors—says AI technologies allow small businesses to be more nimble. To him, AI serves an integral function in his company’s ability to analyze research and data, develop marketing strategies and pitch materials, and share and request information from internal and external partners through tools such as DocuSign and Dropbox.

AI’s ability to present a wealth of knowledge—at a rapid speed—is perhaps equally consequential to those operational efficiency gains. Even for many of Aureate Capital’s clients who may have limited resources to make stock or investment portfolio decisions, AI tools and integrations can assist in the decision-making process or at least help validate their thinking.

It is, therefore, vital for companies to start embracing AI, according to Milliken, if they want to reap these types of benefits for their business and remain competitive.

While applications for AI continue to expand and evolve, one thing is abundantly clear: small businesses that use AI are seeing increased growth and profitability and are better equipped to compete in a dynamic marketplace.

]]>