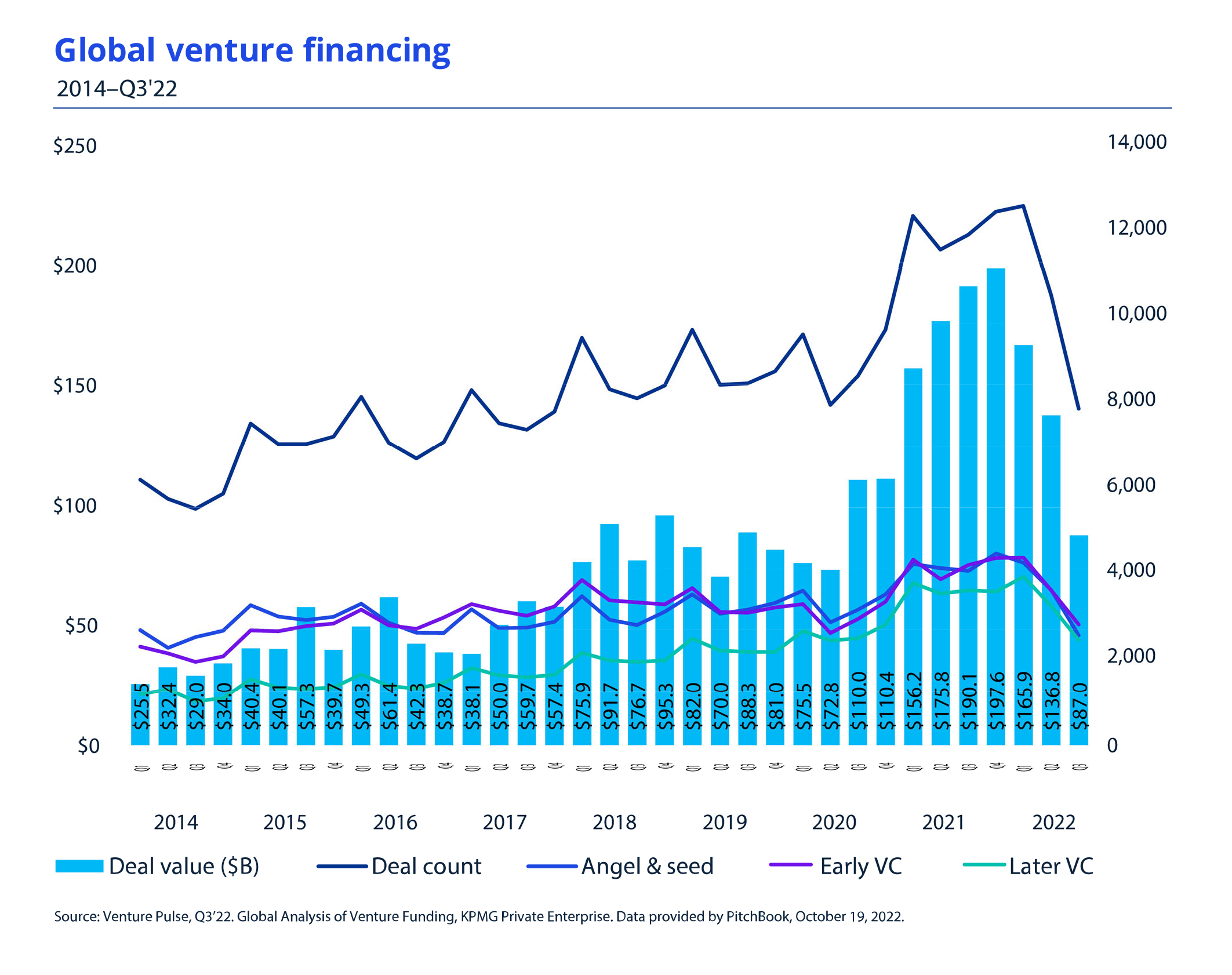

Number of global VC deals plummets to 7,817 in Q3’22—lowest level since Q4’17 and global investment declines for the third consecutive quarter. Deal numbers across the Americas, Europe and Asia drop, with Americas attracting more than half of global VC total, $45.5 billion, during quarter.

![]()

Signs point to Q4 VC funding being lower than hoped as geopolitical turmoil remains while increased due diligence and investor caution cause delays to deals closing.

Amid a growing energy crisis, economic turbulence, continued pandemic impacts and increased pressures on businesses, funds continue to flow into clean energy, fintech, biotech, cyber and B2B, including AI and machine learning start-ups and scale-ups

NEW YORK–(BUSINESS WIRE)–Global VC investment is likely to continue to fall throughout the final quarter of 2022 as Q3 sees the third consecutive drop in deals and funding value whilst signs indicate increased conservativism amongst investors amid rising fears of a global recession.

According to the Q3’22 edition of Venture Pulse — a quarterly report, published by KPMG Private Enterprise, that analyzes key VC deals and trends globally, global VC funding fell to a nine-quarter low of $87 billion in Q3’22; levels not seen since 2020 in the Americas, Europe, and Asia. The decline in the number of deals was even more marked during the quarter, with just 7,817 VC deals globally—the lowest volume since Q4’17.

“Significant market volatility, ongoing geopolitical and economic turmoil – including fears of a recession – have led to a continued and significant cooling of global VC funding,” said Jonathan Lavender, Global Head, KPMG Private Enterprise, KPMG International.

“Despite five deals closing with values over $1 billion, the VC environment has seen the overall number of deals drop to its lowest levels since 2017 and the value of those deals slump to mid-2020 levels; the peak of the pandemic and lockdowns.”

While annual fundraising reached $220 million at the end of Q3’22, on track to rank as the second highest year for fundraising ever next to 2018, VC investors were more critical with their investments, becoming increasingly cautious, placing a laser focus on profitable companies, and those with sustainable business models or market-leading innovators, such as SpaceX which closed $1.9 billion in capital.

Consumer facing companies such as e-commerce and food delivery groups are losing traction amongst investors. Rising inflation, climbing interest rates and recessionary concerns are raising questions about a potential shift in consumer buying behaviours. However, a growing energy crisis – particularly in Europe – the continued effects of the pandemic, and increased pressures on businesses means some sectors remain of high-interest to investors. Clean energy, fintech, biotech, cyber and B2B; including AI and machine learning start-ups and scale-ups, continue to be popular.

Conor Moore Head of KPMG Private Enterprise in the Americas Region & Leader, KPMG Private Enterprise Emerging Giants Network, KPMG International commented: “It’s not doom and gloom for all start-ups and scale-ups however, increased conservatism and caution from investors and an overall tighter landscape may push many to consider alternative financing sources.”

“Late-stage companies have recognized that funding priorities have shifted dramatically and that if they want to attract investment they will need to focus on their profitability story.”

During Q3’22, all major regions attracted at least one $1 billion+ megadeal. As well as US-based SpaceX raising $1.9 billion, Germany-based Celonis raised $1.4 billion, China-based Sunwoda EVB raised $1.2 billion, Sweden-based Northvolt raised $1.1 billion, and US-based TerraWatt Infrastructure raised $1 billion.

Key Highlights – Q3’22

- Global VC investment fell for the third straight quarter, from $136.8 billion in Q2’22 to $87 billion in Q3’22.

- The number of global VC deals dropped from 10,425 in Q2’22 to 7,817 in Q3’22—the lowest level in almost five years.

- The US accounted for $43 billon in VC investment in Q3’22, near half of global total.

- VC investment across the Americas declined from $76.6 billion to $45.6 billion quarter-over quarter.

- VC investment in Asia dropped from $26.6 billion in Q2’22 to $21.7 billion in Q3’22.

- Europe experienced a sharp drop in VC investment between Q2’22 and Q3’22, from $31 billion to $18.7 billion.

- Global corporate affiliated VC investment fell from $59 billion across 2,459 deals in Q2’22 to $40.5 billion across 1,810 deals in Q3’22.

- VC-backed exit value increased from $86.6 billion in Q2’22 to $101.1 billion in Q3’22, driven by a large increase exit value in Asia—from $51.6 billion in Q2’22 to $82 billion in Q3’22. Exit value in the US remained incredibly weak, with $14 billion in exits – the lowest level since Q4’16.

Energy sector attracts big raises in Q3’22

Energy attracted a number of big raises across regions in Q3’22. In China, electric vehicle battery maker Sunwoda EVB raised $1.1 billion, lithium battery company Hubei Rongtong High Advanced Material raised $744 million, intelligent electric vehicle platform company Avatar Technology raised $377 million, and solar power research and manufacturing company Gokin Solar raised $369 million.

In the US, electric vehicle infrastructure company TerraWatt Infrastructure raised $1 billion, nuclear innovation company TerraPower raised $750 million, and ESG commodities marketplace company Xpansiv raised $400 million. While Europe saw mostly smaller deals in the space, Sweden-based EV battery company Northvolt raised $1.1 billion.

Fundraising in Americas has already reached a new annual record high of $156 billion at end of Q3’22

Both VC investment and the number of VC deals tumbled across the Americas, falling from $76.6 billion across 4,607 deals in Q2’22 to $45.6 billion across 3,364 deals in Q2’22. The US attracted the bulk of funding in the region during the quarter ($43 billion). VC investment dropped from $2 billion in Q2’22 to $1.4 billion in Q3’22 in Canada, from $988 million to $516.8 million in Brazil, and from $714 million to $231 million in Mexico.

Despite all this, at the end of Q3’22, total fundraising in the Americas reached $156.2 billion, already eclipsing the previous annual high of $151.9 billion seen in 2021. While the majority of this fundraising occurred in the US, both Canada and Brazil also experienced robust fundraising compared to previous years.

After major drop in Q2’22, VC investment in Asia drops further

VC investment in Asia fell for the third straight quarter in Q3’22, sinking to $21.7 billion. After falling to a multi-year low of $10 billion in Q2’22, VC investment in China rose to $12.9 billion Q3’22. Other jurisdictions, meanwhile, saw VC investment plummet. In India, VC investment dropped more than 50%—from $7.5 billion to $2.6 billion quarter-over-quarter, while VC investment fell from $1.6 billon to $1.2 billion in Japan and from $1.1 billion to $746 million in Australia.

Despite 2 $1 billion+ megadeals, VC investment in Europe falls sharply

Europe saw VC investment sink from $31.1 billion in Q2’22 to $18.7 billion in Q3’22 as a number of jurisdictions saw VC investment fall by 50% or more, including the UK, Israel, and Ireland. Quickly rising interest rates, sharply increasing energy costs, growing concerns about a potential recession, and the ongoing war between Russia and the Ukraine combined to make investors in the region highly cautious during the quarter. Business productivity attracted significant interest from VC investors in Europe during Q3’22, led by a $1.4 billion raise by Germany-based Celonis.

Heading into final quarter of 2022, investor caution only expected to grow

With no end in sight to the global macroeconomic uncertainty VC investment is expected to remain subdued heading into Q4’22 as VC investors only become more cautious. While energy, business productivity, and cybersecurity will likely remain relatively hot tickets for VC investors globally, other sectors could see a major drop-off in interest, including consumer-driven sectors like rapid food and grocery delivery.

Conor Moore added: “Q4’22 will likely look a lot like this one—with depressed valuations, more layoffs, and more down rounds. I also think we’ll start to see more exit activity. While the IPO door is shut pretty tight for the moment, there could be an upswing in M&A activity as mature companies consider alternative exit plans, companies unable to raise new funding look for potential buyers, and buyers continue to look for bargains.”

Notes to Editors

About KPMG Private Enterprise

You know KPMG, you might not know KPMG Private Enterprise. We’re dedicated to working with businesses like yours. It’s all we do. Whether you’re an entrepreneur, a family business, or a fast-growing company, we understand what’s important to you.

The KPMG Private Enterprise global network for Emerging Giants has extensive knowledge and experience working with the startup ecosystem. From seed to speed, we’re here throughout your journey. You gain access to KPMG’s global resources through a single point of contact—a trusted adviser to your company. It’s a local touch with a global reach.

About KPMG International

KPMG is a global organization of independent professional services firms providing Audit, Tax and Advisory services. KPMG is the brand under which the member firms of KPMG International Limited (“KPMG International”) operate and provide professional services. “KPMG” is used to refer to individual member firms within the KPMG organization or to one or more member firms collectively.

KPMG firms operate in 144 countries and territories with more than 236,000 partners and employees working in member firms around the world. Each KPMG firm is a legally distinct and separate entity and describes itself as such. Each KPMG member firm is responsible for its own obligations and liabilities.

KPMG International Limited is a private English company limited by guarantee. KPMG International Limited and its related entities do not provide services to clients.

For more detail about our structure, please visit home.kpmg/governance.

Contacts

For more information and media enquiries:

Daniel Caines, Senior Manager, Global External Communications, KPMG International

T: +44 7732400262

E: Daniel.Caines@kpmg.co.uk